Weekly Power Outlet US - Week 8

Cheniere Energy Announcements, the BASF, and Transmission Line (ROFR).

Energy Market Update Week 8, brought to you by Acumen.

For More Updates Like This, Subscribe Here!Yesterday we published a blog post discussing some trends that may add to volatility in the world of electricity pricing now and in the future. As we’ve covered in these weekly posts as well, given the emergence of natural gas in the generation stack around the US, the price of electricity and natural gas have become highly correlated. One discussion point we’ve noted is how increased LNG export capacity is making the prices more world indexed, much like oil. In almost perfect timing, Cheniere Energy, along with its quarterly earnings release, announced LNG expansion at its Sabine terminal and the resumption of Freeport. The more export capacity the US has, the more our domestic prices will reflect world pricing which tends to be higher.

One danger of developing a thesis is not constantly revisiting it to make sure the logic still adds up. One thing we’ve discussed that could temper LNG exports was reduced demand in Europe. We’ve already seen that this winter with moderate temperatures. Again, we saw perfect timing this morning when German industrial conglomerate BASF announced the closing of two natural gas intensive plants that make synthetics, citing high input cost. Plants in Belgium and the US will increase production as an offset. If industrial demand starts moving to natural gas instead of natural gas being moved, the pace of prices being set by a world market could slow. A single data point doesn’t change our world pricing thesis, but it’s on our radar.

Another issue in volatility has been inadequate transmission to deal with new generation, especially renewables that are far from population centers. We have discussed some of the issues around permitting and land use. One issue that seems to be making headlines more and more are state laws that give incumbent utilities the right of first refusal (ROFR) on new projects. This article from Utility Drive does an excellent job of summarizing some of the issues. Regardless of argument, this is another potential delay in an already arduous process.

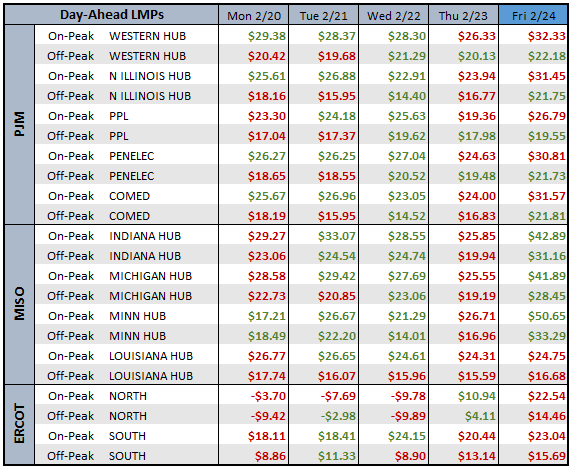

DAY-AHEAD LMP PRICING & SELECT FUTURES

LMPs posted this week looked more like a mild spring week than the middle of February. The calendar On-Peak strips are now trading at $50 or below, after being above $100 last September.

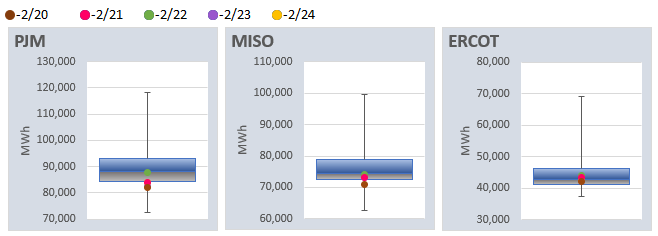

DAILY RTO LOAD PROFILES

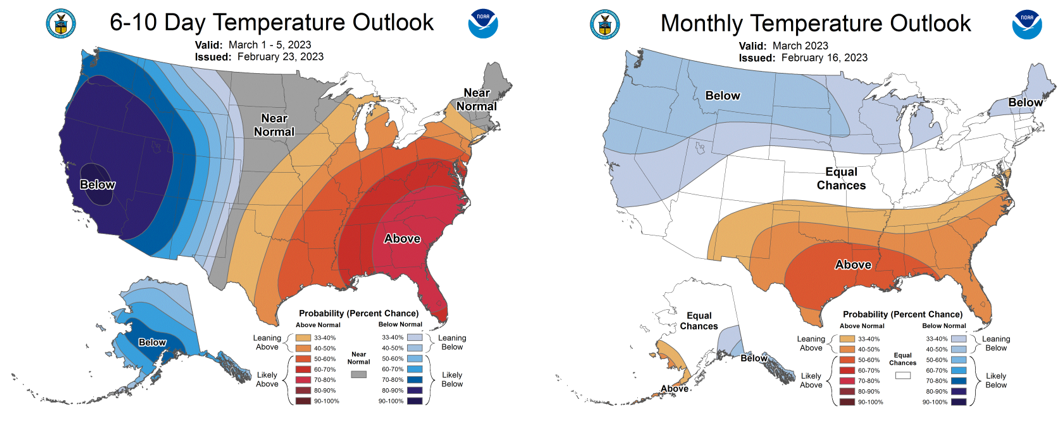

NOAA WEATHER FORECAST

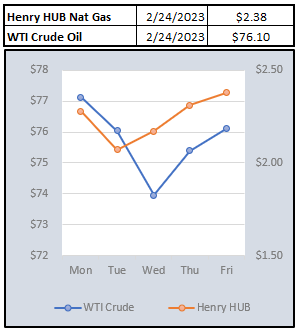

COMMODITIES PRICING

EIA reported a withdrawal of 71Bcf for the previous week. While in-line with estimates, it was well below the five-year average. Midweek saw a bounce in both oil and gas, with some concerns about a stronger pull in gas from the Midwest this week. New England and California both saw spot markets higher, continuing a theme this winter.

Not getting these updates delivered weekly into your inbox? Let's fix that, click the link below: